Cap Rate Is the Most Important Number in Commercial Real Estate

If you want to buy a commercial property, you need to understand one number above everything else: the cap rate. It tells you, at a glance, how much return a property can generate each year relative to its price. Without it, you are essentially buying blind.

In simple terms, the cap rate is the annual return percentage a property produces based on its income and value. Investors use it every single day to compare properties, estimate prices, and decide whether a deal is worth pursuing.

In this guide, you will learn exactly what cap rate means, how to calculate it step by step, what a good cap rate looks like in today’s market, and how to use it to make smarter investment decisions.

What Is Cap Rate on Commercial Property?

Simple Definition

Cap rate, short for capitalization rate, is the percentage return a property generates based on its income alone, with no mortgage factored in. The formula is straightforward:

Cap Rate = Net Operating Income (NOI) ÷ Property Value

For example, if a property earns $100,000 per year in net income and it costs $1,000,000, the cap rate is 10%. That means for every dollar you invest, the property returns 10 cents per year in income.

Why Cap Rate Matters

Cap rate is so widely used because it lets you compare very different properties on a level playing field. A $500,000 property and a $5,000,000 property can both be evaluated using the same percentage. It also serves as a market health indicator , when cap rates are falling, prices are rising, and vice versa. Buyers use it as a pricing benchmark and as a quick risk measure. Whether you are evaluating a rental building in Suffolk County or a mixed-use property in Brooklyn, cap rate gives you an instant, apples-to-apples comparison.

What Cap Rate Is NOT

Before going further, it is important to clear up some common confusion. Cap rate is not your actual investment return, because it ignores your mortgage payments entirely. It is also not the same as:

- Cash-on-cash return (which does include financing)

- Total return (which includes appreciation)

- IRR , Internal Rate of Return (which accounts for the full timeline of an investment)

How to Calculate Cap Rate: Step-by-Step

Step 1: Calculate Net Operating Income (NOI)

NOI is the total income a property produces after paying its operating expenses, but before any mortgage payment. Here is how you build it:

Start with Gross Rental Income

Add up all the rent you collect annually. Include extras like parking fees, storage unit income, and laundry revenue.

Subtract Vacancy Loss

Most properties are not rented 100% of the time. Subtract a vacancy allowance of around 5% to 10% to reflect realistic occupancy.

= Effective Gross Income

Subtract Operating Expenses

These are the real costs of running the property:

- Property taxes

- Insurance

- Utilities (if you pay them, not the tenants)

- Maintenance and routine repairs

- Property management fees (typically 8–10% of rent)

- Reserves for future capital expenditures

What NOT to Include

Do not include your mortgage payments. Do not include depreciation, capital improvements, or income taxes. These are not operating expenses and will distort your NOI calculation.

= Net Operating Income (NOI)

Step 2: Divide NOI by Property Value

Once you have your NOI, divide it by the purchase price or current market value. Multiply by 100 to get your percentage.

Cap Rate % = (NOI ÷ Value) × 100

Real Example: 10-Unit Apartment Building

| Item | Amount |

|---|---|

| Gross Rental Income | $120,000 |

| Minus Vacancy (5%) | −$6,000 |

| Effective Gross Income | $114,000 |

| Minus Operating Expenses | −$44,000 |

| Net Operating Income (NOI) | $70,000 |

| Purchase Price | $1,000,000 |

| Cap Rate | 7% |

What Is a Good Cap Rate for Commercial Property?

There is no single answer to this question. A good cap rate depends on the property type, its location, the current interest rate environment, and your personal investment goals. Here is a breakdown of typical cap rate ranges in the 2024–2026 market:

Cap Rate Ranges by Property Type

| Property Type | Class / Description | Cap Rate Range |

|---|---|---|

| Multifamily | Class A (newer, prime) | 4–5.5% |

| Multifamily | Class B (good condition) | 5.5–7% |

| Multifamily | Class C (older, value-add) | 7–9% |

| Retail | Single-tenant net lease | 5–6.5% |

| Retail | Neighborhood shopping center | 6–8% |

| Retail | Strip mall | 7–9% |

| Office | Class A (downtown) | 5–7% |

| Office | Suburban Class B | 7–9% |

| Office | Class C | 9–11% |

| Industrial | Institutional logistics | 4.5–6% |

| Industrial | Smaller industrial | 6–8% |

| Industrial | Flex space | 7–9% |

Factors That Influence What Makes a Cap Rate “Good”

Location Premium

Where a property sits has a massive impact. In top-tier primary markets like New York City, cap rates tend to fall between 4% and 6%. Buyers accept lower returns because those cities offer stability and strong demand. This is just as true for residential investors in areas like Nassau County or Queens , location drives value in every property type. In secondary markets, cap rates typically run from 6% to 8%. In smaller tertiary markets, you will often see 8% to 10% or higher.

Risk vs. Return Trade-Off

Lower cap rates generally mean lower risk. The property is stable, well-located, and in high demand, so buyers are willing to pay more for it. Higher cap rates suggest higher risk , vacancies, deferred maintenance, or a declining tenant base. If you are dealing with a distressed or damaged property, you can learn more about how to sell a damaged house and what that means for pricing and return expectations.

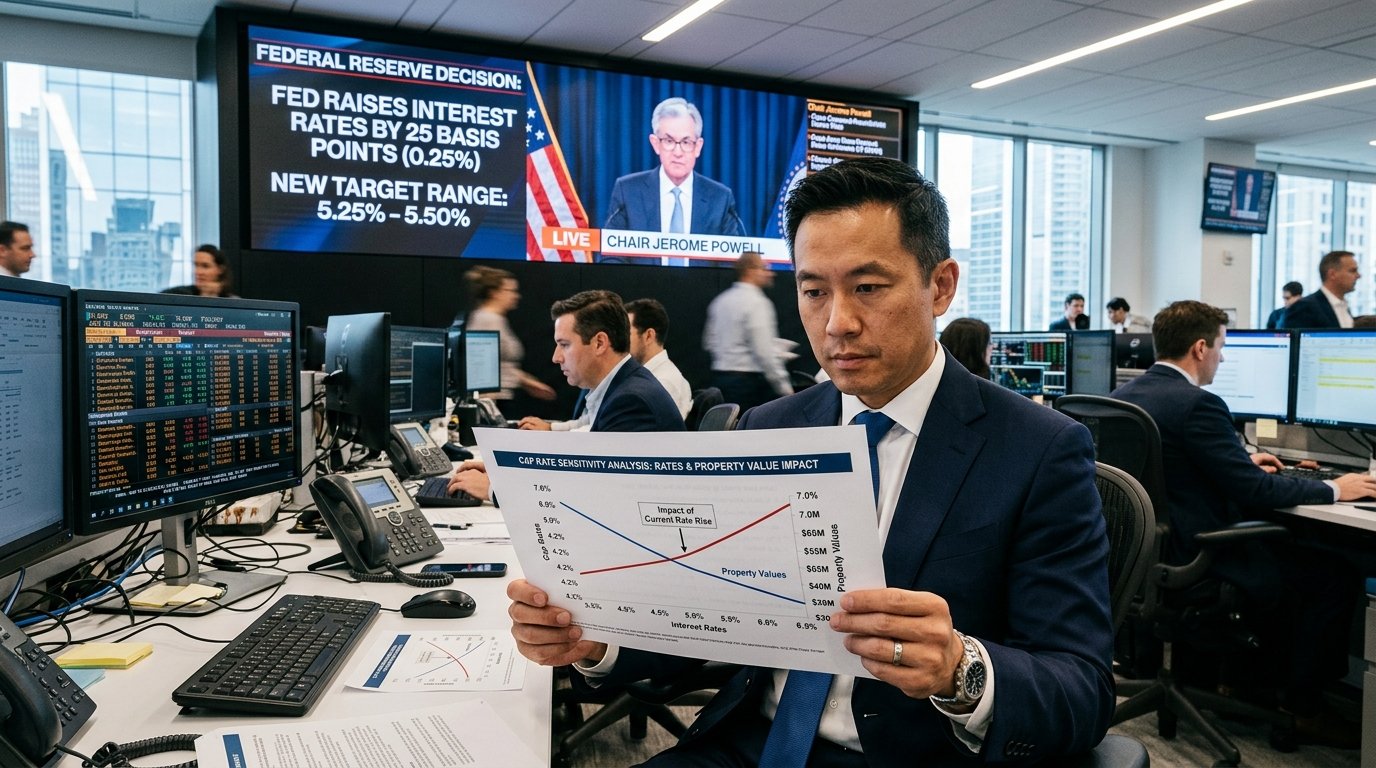

Interest Rate Environment

Cap rates and interest rates tend to move together. When borrowing costs rise, investors need higher returns to make deals work, so cap rates rise and property values fall. When interest rates drop, more money chases real estate, cap rates compress, and values climb.

Your Investment Goals

A conservative investor focused on stable income might be happy with a 5% to 7% cap rate on a well-maintained property. A value-add investor looking to improve a building and increase rents might require 8% to 10% or more. An investor focused on long-term appreciation in a growing market might accept a lower cap rate today in exchange for higher future gains.

Cap Rate and Property Valuation: The Direct Relationship

One of the most powerful uses of cap rate is estimating what a property is actually worth. When you rearrange the formula, you get:

Property Value = NOI ÷ Cap Rate

This means if a property produces $100,000 in NOI and the market cap rate for that property type and location is 8%, the estimated value is $1,250,000. If the market shifts and that same cap rate compresses to 6%, the property would be worth $1,670,000, even though the income did not change at all.

Understanding this relationship is critical whether you are a seasoned investor or a homeowner trying to figure out how much you lose selling a house as-is versus at full market value.

Cap Rate Compression vs. Cap Rate Expansion

Cap rate compression happens when more buyers compete for properties, pushing prices up and cap rates down. Industrial and multifamily real estate experienced dramatic cap rate compression from 2020 through 2024 as investor demand surged.

Cap rate expansion is the opposite. Fewer buyers, less demand, lower prices, higher cap rates. Office properties have gone through painful cap rate expansion since 2023 as remote work reduced demand and many tenants downsized.

How to Use This for Pricing

Find the current market cap rate for your property type and location by looking at recent comparable sales. Calculate your property’s NOI. Then divide to estimate value. This is the same method professional appraisers and brokers use every day. If you are deciding between listing with an agent or selling directly, reading this Long Island agent vs. cash buyer guide can help you weigh your options based on real numbers.

Advanced Cap Rate Analysis

Going-In Cap Rate vs. Exit Cap Rate

The going-in cap rate is what you are buying at today. The exit cap rate is what you project buyers will pay when you eventually sell, typically five to ten years from now. This matters a great deal for calculating your projected IRR. If you buy at a 9% cap and the market improves so that buyers later pay prices implying a 7% cap, you generate significant appreciation on top of your income.

The Cap Rate Compression Play

Some investors deliberately buy properties with high cap rates in markets or property types they believe will improve. The strategy works like this: buy at a 9% cap, improve the property and grow NOI, then sell at a 7% cap as the market stabilizes. The combination of increased income and a compressed cap rate can produce massive gains. The risk is that the market does not cooperate, and cap rates stay high or expand further.

Value-Add Strategy Using Cap Rate

A value-add investor might buy a property at a market cap rate of 8% that currently underperforms due to below-market rents or high vacancies. After renovating units, improving management, and raising rents to market level, the NOI increases by 30%. When sold at a stabilized 7% cap, the investor profits from both the income improvement and the cap rate change. This same logic applies to residential fixer-uppers , if you are wondering whether renovation makes sense before a sale, see how to sell a fixer-upper house fast for a practical breakdown.

Stabilized vs. Unstabilized Cap Rates

A stabilized cap rate reflects a property at full occupancy with market-rate rents. An unstabilized cap rate reflects current performance, which may be lower due to vacancies or below-market leases. When sellers show you a pro forma cap rate, they are projecting future stabilized income. Always verify whether you are looking at actual current performance or optimistic projections.

Common Cap Rate Mistakes Investors Make

Mistake #1: Comparing Apples to Oranges

A 7% cap rate on a Class C apartment building in a rural town is not the same as a 7% cap rate on a well-leased office building downtown. Different property types and locations have completely different risk profiles, even at identical cap rates. Always compare within the same category.

Mistake #2: Trusting Broker Pro Formas

Brokers are paid to sell properties. Their income projections are often optimistic and their expense estimates are frequently too low. Always rebuild the NOI yourself from actual leases, current tax bills, real insurance quotes, and conservative vacancy assumptions. If you are thinking about whether to use an agent at all, consider reading about saving 6% commission by selling without a realtor.

Mistake #3: Ignoring CapEx Reserves

Many investors forget to include reserves for capital expenditures like roofs, HVAC systems, parking lots, and plumbing. Skipping this line inflates NOI and makes the cap rate look better than it really is. A good rule of thumb is to reserve 5% to 10% of gross income for future capital needs.

Mistake #4: Chasing High Cap Rates

A 12% cap rate sounds fantastic until you discover the building has serious structural problems, the neighborhood is declining, or the major tenant is about to leave. High cap rates often exist for very good reasons. Do the work to understand why before assuming it is a bargain. This is especially true for properties with fire or structural damage , understanding how to sell a home with fire damage gives you a realistic picture of the discount buyers will demand.

Mistake #5: Focusing Only on Cap Rate

Cap rate is a starting point, not a finish line. It tells you nothing about your financing costs, your actual cash flow after debt service, the property’s appreciation potential, or the total return over your holding period. Smart investors use cap rate alongside cash-on-cash return, DSCR, and projected IRR to get the full picture.

How to Use Cap Rate in Your Investment Decision

Initial Screening Tool

Before you dig into any deal deeply, set a minimum cap rate threshold that fits your strategy. If you need a 7% cap to make your numbers work, filter out everything below that level immediately. This saves enormous time.

Comparative Analysis

Once you have a property under consideration, compare its cap rate to recent comparable sales in the same market. If the subject property is priced at a lower cap rate than comparable buildings, it is priced at a premium and you need a compelling reason to justify paying it. If it is priced at a higher cap rate, it may be a discount opportunity or it may have problems worth investigating. Investors targeting Long Island markets can explore specific areas like Huntington, Islip, or Brentwood to get a feel for local pricing trends.

Return Requirements

Work backwards from what you need. If your lender requires a debt service coverage ratio of 1.25 and your loan has a certain interest rate, you can calculate the minimum cap rate that lets you hit that target. Similarly, if you want a minimum 8% cash-on-cash return with 70% leverage, you can figure out the cap rate required to achieve it.

Negotiation Leverage

Cap rate analysis gives you concrete, data-driven ammunition in price negotiations. When you can show a seller that comparable properties are trading at a 7.5% cap and their asking price implies a 6% cap, you have a legitimate, professional basis for your offer. This is especially useful in complex sale situations , for example, if a property is being sold due to divorce or estate matters. You can read more about selling a house during divorce and selling an inherited property to understand how motivated sellers may price differently.

Frequently Asked Questions

What is a cap rate in simple terms?

It is the annual income a property produces divided by its price, expressed as a percentage. A 7% cap rate means the property earns 7 cents for every dollar it costs, before any mortgage payments.

How do you calculate cap rate?

Divide the property’s Net Operating Income by its value, then multiply by 100. For example, $70,000 NOI divided by $1,000,000 value equals a 7% cap rate.

What is a good cap rate for commercial property in 2026?

It depends on the property type and location. Multifamily in strong markets often trades at 5% to 7%. Industrial properties range from 4.5% to 8%. Office can run from 5% to 11% depending on class and location. There is no single universal answer.

Is a 7% cap rate good?

In most markets and property types, yes, a 7% cap rate is considered a solid, middle-of-the-road return. It suggests reasonable stability without being so low that there is no yield cushion. Context still matters , a 7% cap in a declining market is very different from one in a stable, growing area.

What does a 10% cap rate mean?

A 10% cap rate means the property generates annual income equal to 10% of its purchase price. It typically signals a higher-risk property or a less desirable location. The return is higher, but so is the potential for problems.

Why are cap rates different for different properties?

Because risk levels differ. A brand-new apartment complex with long-term leases in a major city carries far less risk than an older strip mall in a small town. Investors demand higher returns for taking on more risk, which pushes cap rates up on riskier assets.

What is the relationship between cap rate and property value?

They move in opposite directions. When cap rates fall, property values rise. When cap rates rise, property values fall. A lower cap rate means buyers are willing to pay more for each dollar of income.

Is a higher cap rate better?

Not automatically. Higher cap rates come with higher risk. A higher cap rate can mean better current income, but it might also signal vacancy problems, location challenges, or deferred maintenance. It depends entirely on why the cap rate is high.

What is cap rate vs. ROI?

Cap rate measures income return on property value without considering financing. ROI is a broader measure that can include all forms of return, including appreciation and the effect of leverage. They are related but not interchangeable.

How does interest rate affect cap rate?

When interest rates rise, investors need higher returns to justify buying real estate over bonds and other instruments, so cap rates typically rise and prices fall. When rates fall, real estate becomes relatively more attractive, buyers accept lower cap rates, and values increase.

What is a good cap rate for multifamily?

In 2025–2026, Class A multifamily in primary markets trades at roughly 4% to 5.5%. Class B properties fall around 5.5% to 7%. Class C value-add properties typically see 7% to 9% cap rates.

What is cap rate compression?

It occurs when market demand drives prices up faster than income growth, causing cap rates to decrease. When a market compresses from 8% to 6%, a property that earned $100,000 annually jumps in value from $1.25 million to $1.67 million.

How to increase cap rate on your property?

Increase NOI by raising rents to market level, reducing vacancies, adding income sources, or cutting operating expenses. Since cap rate = NOI / value, growing income without proportionally growing costs improves the cap rate.

What is stabilized cap rate?

It is the cap rate based on a property at full, sustainable occupancy with market-rate rents , its optimal operating condition. Sellers often use it to show what the property will earn once any current issues are resolved.

What expenses are included in cap rate calculation?

Property taxes, insurance, utilities (if owner-paid), maintenance, property management fees, and capital expenditure reserves. Mortgage payments and depreciation are NOT included.

Is cap rate the same as cash-on-cash return?

No. Cap rate ignores financing. Cash-on-cash return measures the actual cash income you receive after making your mortgage payment, divided by the cash you invested. They can be very different numbers depending on your loan terms.

Why do Class A properties have lower cap rates?

Because they are considered low-risk. Institutional investors and REITs compete heavily for high-quality assets, driving up prices. Lower risk means buyers accept lower returns, which equals a lower cap rate.

What is exit cap rate?

It is the cap rate you project buyers will use when you eventually sell the property. If you assume the market will compress from 8% to 7% over your holding period, that assumption , the exit cap , significantly affects your projected IRR.

How do you find market cap rates?

Look at recent comparable sales in your target market and property type. Commercial brokers, appraisers, real estate data services, and published market reports from firms like CBRE, JLL, or Marcus & Millichap all track and report market cap rates regularly.

What is cap rate expansion?

The opposite of compression , when cap rates rise, meaning prices fall relative to income. This typically happens when demand weakens, interest rates rise, or a specific property type falls out of favor, as happened with office buildings after 2022.

Should I buy a property with a 5% cap rate?

Possibly. A 5% cap rate in a prime multifamily market with strong rent growth potential may be an excellent long-term investment. The same cap rate on a struggling retail center in a declining market probably is not. Your financing cost, growth assumptions, and investment timeline all matter.

What is pro forma cap rate?

It is a projected cap rate based on estimated future income, not current actual performance. Sellers and brokers use pro forma cap rates to show what a property could earn after improvements or lease-up. Always verify the assumptions behind any pro forma.

How does cap rate relate to 1031 exchange?

Investors completing a 1031 exchange often face pressure to buy quickly to avoid paying capital gains tax. In a 1031 scenario, understanding the target property’s cap rate is critical to ensure the replacement property meets your return requirements and is not overpriced in the rush to close.

Can cap rate be negative?

Technically yes, but it would mean the property’s operating expenses exceed its income , it has a negative NOI. This can happen temporarily during a major renovation or in periods of severe vacancy. A negative cap rate is a serious red flag in normal operating conditions.

How to calculate NOI for cap rate?

Start with total gross rental income. Subtract a vacancy factor (5–10%). Then subtract all operating expenses including taxes, insurance, utilities, maintenance, management fees, and capital reserves. The result is your NOI.

Conclusion

Cap rate is one of the most powerful tools in commercial real estate. It lets you quickly screen deals, compare properties side by side, estimate market value, and negotiate from a position of knowledge. A good cap rate is not a fixed number , it is the one that makes sense for your market, your property type, and your investment goals.

Start every analysis by calculating the real NOI. Understand the market cap rates for your target asset class. Know what you need to make your deal work financially. And never mistake a high cap rate for a guaranteed winner , always dig into why it is high.

Ready to analyze your next deal? Use the valuation framework covered here alongside a full property due diligence checklist to make sure every number you are working with is real. And if you are weighing whether to hold, sell, or exit a property quickly, explore your options at We Buy Property NY , whether you are dealing with an inherited property, a home in foreclosure, or simply want to sell your house fast.